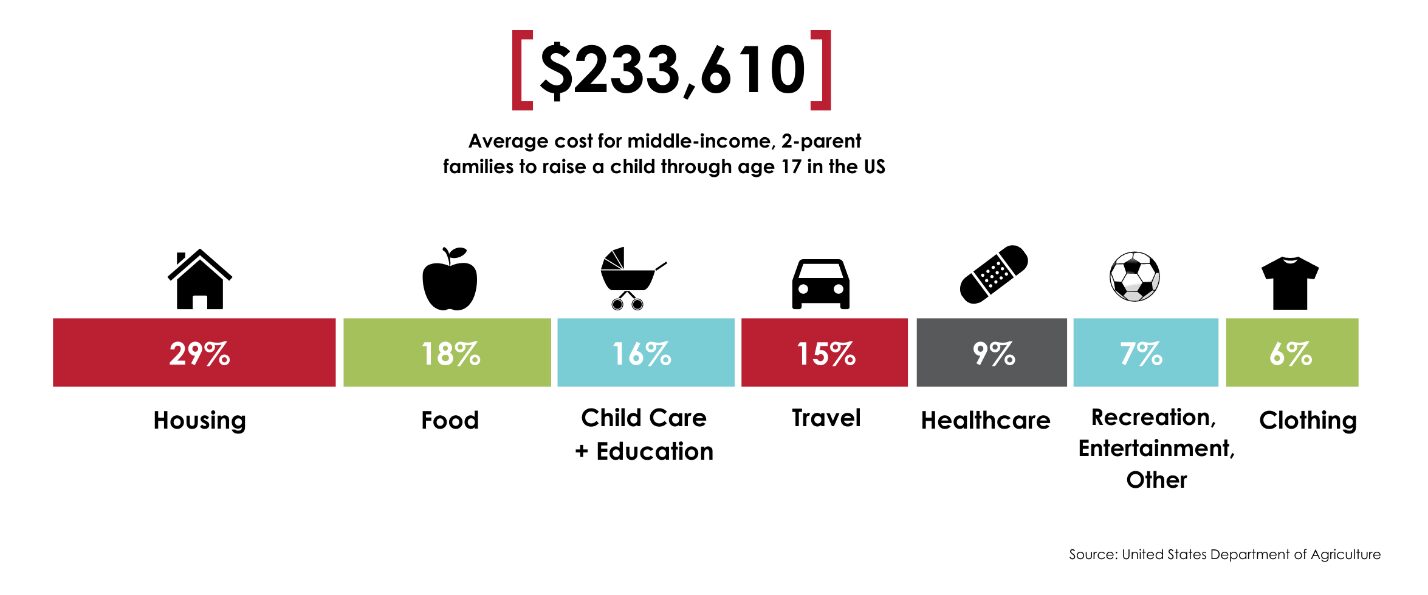

With a baby comes one of life’s biggest joys, but they also comes with a lot of new expenses. In the US, the average cost of raising a child through the age of 17 is $233,610. This figure is based on the most recent ‘Expenditures on Children by Families’ report completed by the United States Department of Agriculture (USDA).

Beyond the purchase of items such as a crib, diapers and car seat; here are some additional financial items to think about to help you prepare for the arrival of your new family member.

The first month of your baby’s life may be the priciest, because it includes maternity care, the cost of delivery, postnatal care, and a hospital stay. The numbers can vary depending on where you live, if you are giving birth or adopting, and your insurance policy.

Understand your maternity/paternity leave

It’s important to familiarize yourself and understand your workplace’s maternity and paternity leave policies. You’ll want to look into how much leave is offered and how much of your salary will you be paid during that time.

Review Insurance Policies

Having a baby is expensive, even when you have health insurance, so you’ll want to check your policy to see what is covered and what is out of pocket. Keep in mind that the cost of routine birthing care is variable based on your insurance coverage so you will want to review your policy to find out what your out-of-pocket costs are for prenatal care, tests, hospital stay, and postpartum.

Make sure you know what it costs to add an additional dependent to your health insurance policy, and how you long you have from child’s birth date to add them. (It’s recommended to do it sooner rather than later). Plan on around 6 wellness visits for evaluations, immunizations, etc., and possibly a few additional visits for illnesses for your baby in the first year. If possible, make you stay in-network while choosing your child’s pediatrician, as well as avoid going outside of your network of hospitals to avoid paying additional costs.

Life Insurance: This is also a good time to review or modify your life insurance policies. Assuming you already have life insurance, you may want to review or consider adding policies for medical, dental, and disability. During this time you may want to add your child as a beneficiary on your policy (same for your 401(k) and IRAs as well). Keep in mind that you’ll need to make adjustments elsewhere, such as a will or trust, to ensure when, and how, your child will have access to the money.

Adjust your current budget to accommodate your new baby

Babies come with a lot of expenses, including instant and longer term ones. A great tool for approximating first year costs is the cost calculator at BabyCenter.com. This tool takes into account one time and ongoing items, such as a car seats, diapers, clothing, daycare etc. This tool can be very helpful when accounting for these items while creating your monthly and yearly budget. To monitor your new expenses and adjust your budget in real time, you can easily access your account activity online.

Your exact expenses during your child’s life will depend on choices like school, childcare and lifestyle. While you are budgeting, try to look ahead to be able to plan for both your short and long-term financial goals.

Additional tip: If you are planning to have a baby shower, be practical about your baby registry. If you can wait, don’t go baby shopping till after. You will most likely get a lot of items at your shower, and you can put the money you would have otherwise spent on these items towards filling in the gaps of what you still need and your financial saving goals.

Other ways to save:

- Babies grow fast! Buying clothes secondhand can save you a good amount of money

- Buying in bulk, using cash-back apps and ‘couponing’ can cut your budget

- Prepare your own baby food at home to help with food costs when baby starts getting introduced to food other than formula or breast milk. Here is a Step-By-Step Guide to Making Baby Food by verywellfamily.com

18 and beyond:

Savings Account: Consider starting to save for long-term expenses as your baby grows. Set up a savings account for your baby (check out our Good Savers Account that is specific for children). Putting away a specific percentage of your paycheck each month can help you build up this savings.

Continuing education: Starting early in your child’s life allows you to leverage time to build up nice savings for your child’s post-high school education. If your child decides to go to college, the current average cost of a full-time undergraduate, per year according to Education Data (2019-2020), is roughly estimated at $30,500.

Parents who choose to help pay for college can take advantage of savings plans like the 529 College Savings Plans. A 529 plan is a state sponsored plan that allows families to save specifically for college costs. As long as the money is used to pay for college expenses, the withdrawals are free of federal taxes. If you start a 529 plan, and your child decides not to go to college, the money may be used for another child or withdrawn, subject to tax and penalties. A bonus of these plans is that family and friends can contribute to your child’s 529 plan for easy gift ideas for birthdays and holidays.

Overall, planning for a child is an exciting time. By preparing for these financial items in addition to dreaming of what their eye color is going to be, it will allow you more time to enjoy your new addition to your family.